(Please click on the image above to view our short YouTube video)

(Please click on the image above to view our short YouTube video)

Our local real estate market experts, Market Watch LLC, have just released their Desert Housing Report for March 2022. Some highlights:

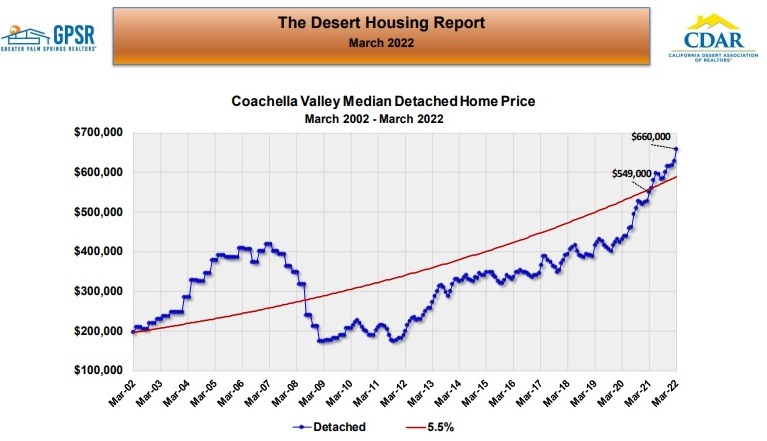

Coachella Valley Detached Home Median Price: At the end of March, the Coachella Valley detached home median price was $660,000 (up 20.2% year-over-year from $549,000 at the end of March 2021). Market Watch felt that if the historical seasonal detached home price pattern applies, then detached home prices should continue to increase over the next two months, then soften somewhat. They felt that the forces that have been driving detached home prices higher, i.e., low inventory and high demand, continue to dominate the market.

Coachella Valley Detached Home Median Price: At the end of March, the Coachella Valley detached home median price was $660,000 (up 20.2% year-over-year from $549,000 at the end of March 2021). Market Watch felt that if the historical seasonal detached home price pattern applies, then detached home prices should continue to increase over the next two months, then soften somewhat. They felt that the forces that have been driving detached home prices higher, i.e., low inventory and high demand, continue to dominate the market.

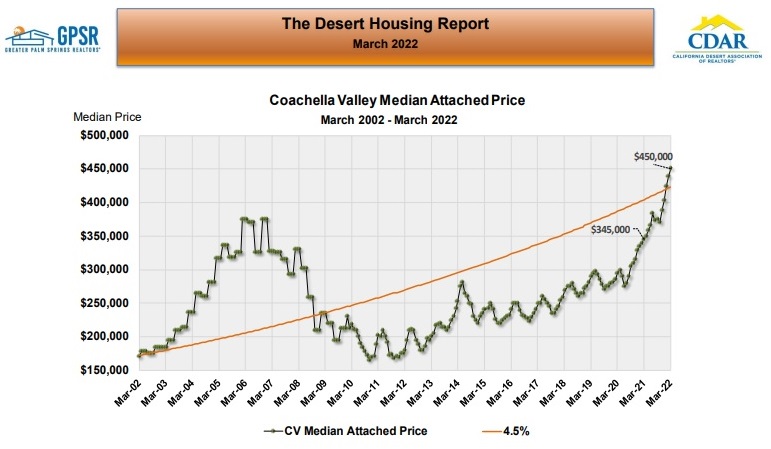

Coachella Valley Attached Home Median Price: At the end of March, the Coachella Valley attached home median price was $450,000 (up 30.4% year-over-year from $345,000 at the end of March 2021). Market Watch noted that the attached home median price has surged more than 50% over the last two years. Further, they felt that if the historical seasonal attached home price pattern applies, then attached home prices should peak sometime in the next two months and then soften.

Coachella Valley Attached Home Median Price: At the end of March, the Coachella Valley attached home median price was $450,000 (up 30.4% year-over-year from $345,000 at the end of March 2021). Market Watch noted that the attached home median price has surged more than 50% over the last two years. Further, they felt that if the historical seasonal attached home price pattern applies, then attached home prices should peak sometime in the next two months and then soften.

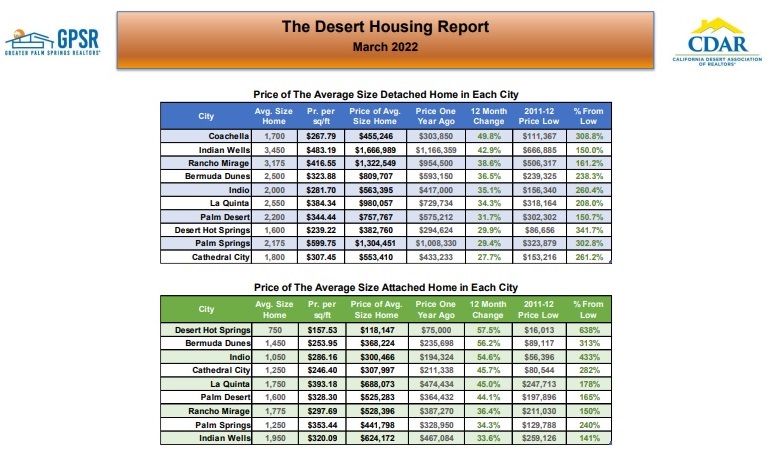

Twelve Month Change in The Price of The Average Size Home By City: The median price of the average size detached home increased by more than 40% year-over-year in Coachella (for the average 1,700 sq ft Coachella detached home) and Indian Wells (for the average 3,450 sq ft Indian Wells detached home). The median price of the average size detached home increased by more than 30% year-over-year in Rancho Mirage (for the average 3,175 sq ft Rancho Mirage detached home), Bermuda Dunes (for the average 2,500 sq ft Bermuda Dunes detached home), Indio (for the average 2,000 sq ft Indio detached home), La Quinta (for the average 2,550 sq ft La Quinta detached home) and Palm Desert (for the average 2,200 sq ft Palm Desert detached home). The attached home median price increased by more than 50% year-over-year in Desert Hot Springs (for the average 750 sq ft Desert Hot Springs attached home), Bermuda Dunes (for the average 1,450 sq ft Bermuda Dunes attached home) and Indio (for the average 1,050 Indio attached home). The attached home median price increased by more than 40% year-over-year in Cathedral City (for the average 1,250 sq ft Cathedral City attached home), La Quinta (for the average 1,750 sq ft La Quinta attached home) and Palm Desert (for the average 1,600 sq ft Palm Desert attached home).

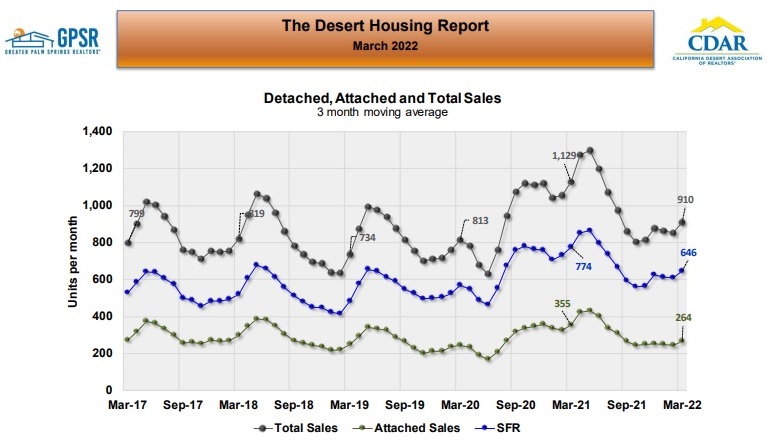

Monthly Home Sales – Three-Month Trailing Average: Three-month total home sales in March averaged 910 home per month (down 19.4% from 1,129 average home sales in March 2021). Market Watch noted that while total home sales were below the peak home sales levels of last year, home sales in March continued to average significantly higher that pre-pandemic March averages (813 average total home sales in March 2020 and 734 average total home sales in March 2019). Market Watch concluded that while Coachella Valley housing inventory remains tight, buyer demand for housing in the Coachella Valley remains strong.

Monthly Home Sales – Three-Month Trailing Average: Three-month total home sales in March averaged 910 home per month (down 19.4% from 1,129 average home sales in March 2021). Market Watch noted that while total home sales were below the peak home sales levels of last year, home sales in March continued to average significantly higher that pre-pandemic March averages (813 average total home sales in March 2020 and 734 average total home sales in March 2019). Market Watch concluded that while Coachella Valley housing inventory remains tight, buyer demand for housing in the Coachella Valley remains strong.

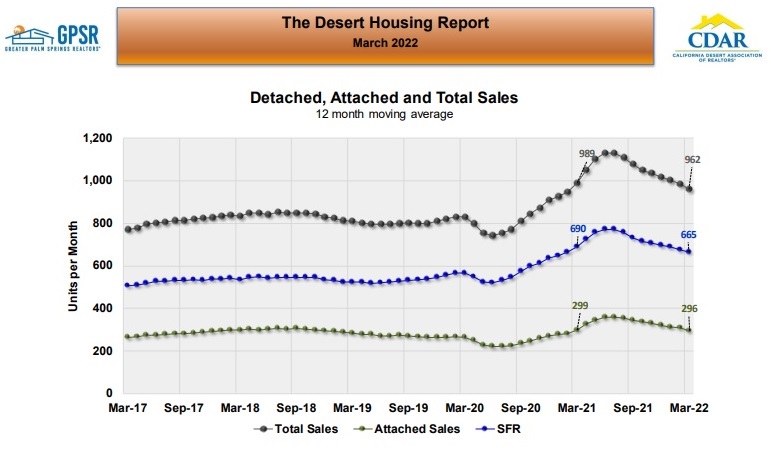

Monthly Home Sales – Twelve-Month Trailing Average: Twelve-month home sales in March (which takes out all seasonality in home sales data) averaged 962 units a month (down 2.7% from 989 total homes sales in March 2021). Sales of detached homes were down 3.6%, while sales of attached homes were almost unchanged. Market Watch expects long term home sales to continue to retreat from the highs in June 2021 because of supply restrictions due to low housing inventory.

Monthly Home Sales – Twelve-Month Trailing Average: Twelve-month home sales in March (which takes out all seasonality in home sales data) averaged 962 units a month (down 2.7% from 989 total homes sales in March 2021). Sales of detached homes were down 3.6%, while sales of attached homes were almost unchanged. Market Watch expects long term home sales to continue to retreat from the highs in June 2021 because of supply restrictions due to low housing inventory.

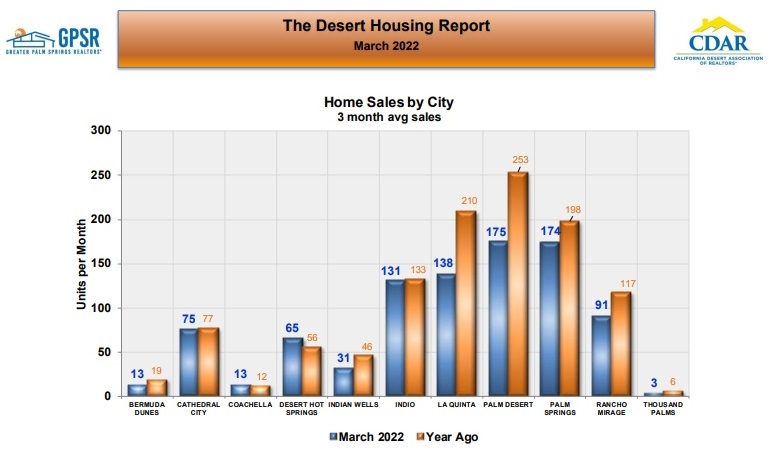

Home Sales by City: Market Watch noted that the largest decline in home sales year-over-year in March continued to be in the four major resort cities of La Quinta, Palm Desert, Palm Springs and Rancho Mirage. Those Coachella Valley cities classified primarily as “work force” cities, i.e., Cathedral City, Desert Hot Springs and Indio, continued to show increased average March home sales compared to last year.

Home Sales by City: Market Watch noted that the largest decline in home sales year-over-year in March continued to be in the four major resort cities of La Quinta, Palm Desert, Palm Springs and Rancho Mirage. Those Coachella Valley cities classified primarily as “work force” cities, i.e., Cathedral City, Desert Hot Springs and Indio, continued to show increased average March home sales compared to last year.

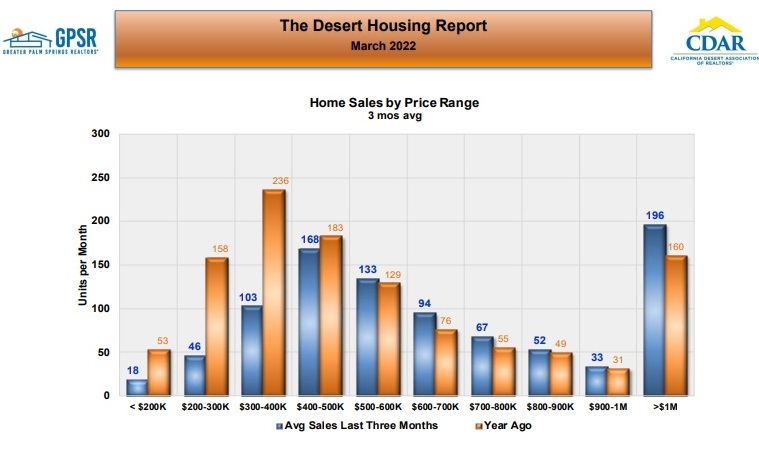

Home Sales by Price Range: Market Watch pointed out the significant decline in sales of homes priced under $400,000 in March and the slight increase in sales of homes priced over $500,000 in March. Most of this increase is simply due to more homes being in those higher price brackets. Market Watch noted the 196 sales of homes priced over a million dollars in March (a three-fold increase over the 72 sales of homes priced over one million dollars in March 2020).

Home Sales by Price Range: Market Watch pointed out the significant decline in sales of homes priced under $400,000 in March and the slight increase in sales of homes priced over $500,000 in March. Most of this increase is simply due to more homes being in those higher price brackets. Market Watch noted the 196 sales of homes priced over a million dollars in March (a three-fold increase over the 72 sales of homes priced over one million dollars in March 2020).

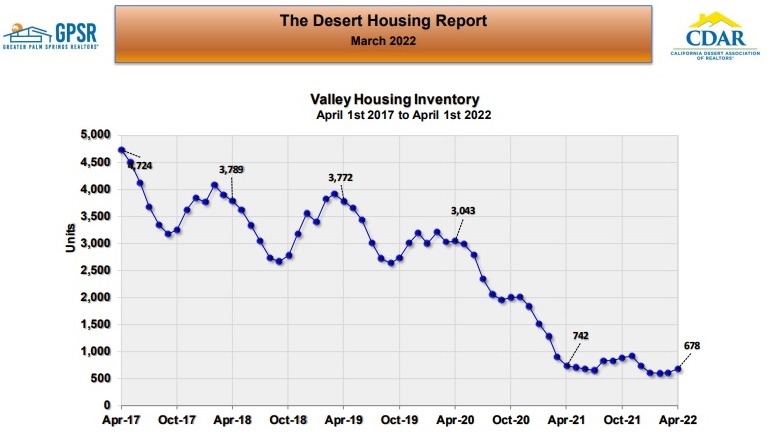

Coachella Valley Total Housing Inventory: On April 1st, the Coachella Valley total housing inventory was 678 homes (down 8.6% from April 1st 2021 and down 77.7% from April 1st 2020). Market Watch noted the absence of the usual seasonal rise in housing inventory between October and April points to even lower inventory moving toward September. Market Watch felt that it would take a surge in listings to increase inventory, but with only 1,244 new listings in March (which is just an average amount), Market Watch didn’t see it happening yet.

Coachella Valley Total Housing Inventory: On April 1st, the Coachella Valley total housing inventory was 678 homes (down 8.6% from April 1st 2021 and down 77.7% from April 1st 2020). Market Watch noted the absence of the usual seasonal rise in housing inventory between October and April points to even lower inventory moving toward September. Market Watch felt that it would take a surge in listings to increase inventory, but with only 1,244 new listings in March (which is just an average amount), Market Watch didn’t see it happening yet.

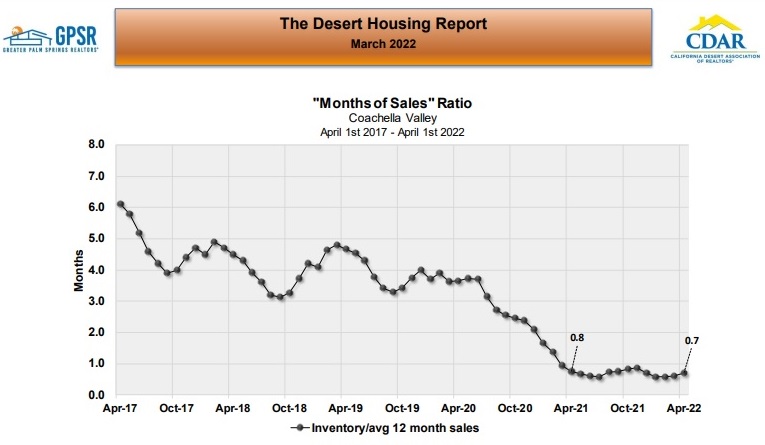

Coachella Valley Overall Months of Sales Ratio: On April 1st, the months of sales ratio for the entire Coachella Valley was 0.7 months (down from 0.8 months on April 1st, 2021). These historically low months of sales ratios continue to indicate extremely low supply and moderate to strong buyer demand, which are the two ingredients for higher prices. Market Watch felt that even though Coachella Valley home prices have surged, the months of sales ratio is a strong indication that home prices will continue to trend higher.

Coachella Valley Overall Months of Sales Ratio: On April 1st, the months of sales ratio for the entire Coachella Valley was 0.7 months (down from 0.8 months on April 1st, 2021). These historically low months of sales ratios continue to indicate extremely low supply and moderate to strong buyer demand, which are the two ingredients for higher prices. Market Watch felt that even though Coachella Valley home prices have surged, the months of sales ratio is a strong indication that home prices will continue to trend higher.

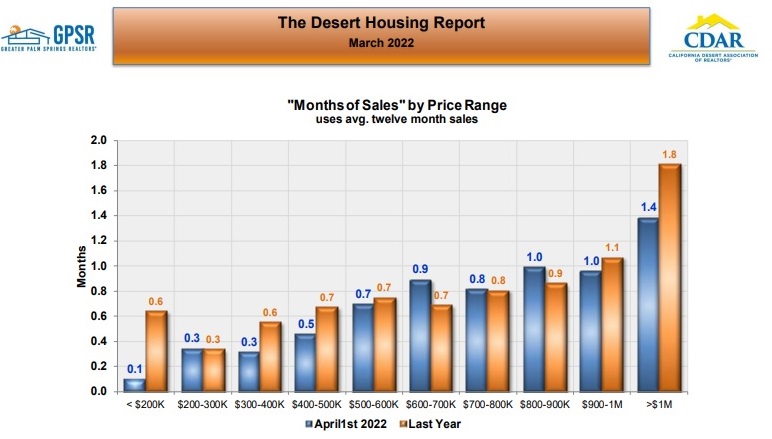

Months of Sales by Price Range: The months of sales ratio in every price bracket under $600,000 was less than, or equal to, year ago levels. The months of sales ratio for homes priced from $600,000 to $900,000 was slightly higher, or equal to, year ago levels. For homes over $900,000, the months of sales ratios were less than last year.

Months of Sales by Price Range: The months of sales ratio in every price bracket under $600,000 was less than, or equal to, year ago levels. The months of sales ratio for homes priced from $600,000 to $900,000 was slightly higher, or equal to, year ago levels. For homes over $900,000, the months of sales ratios were less than last year.

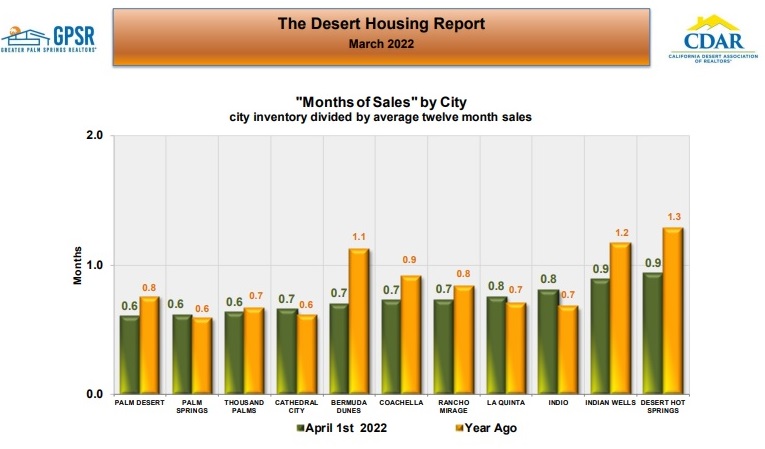

Months of Sales by City: The Coachella Valley cities with the lowest months of sales ratios on April 1st were Palm Desert, Palm Springs and Thousand Palms at 0.6 of a month. Market Watch felt that what was particularly noteworthy was how close the moths of sales ratios were in all of the Coachella Valley cities (with months of sales ratios between 0.6 and 0.9 months).

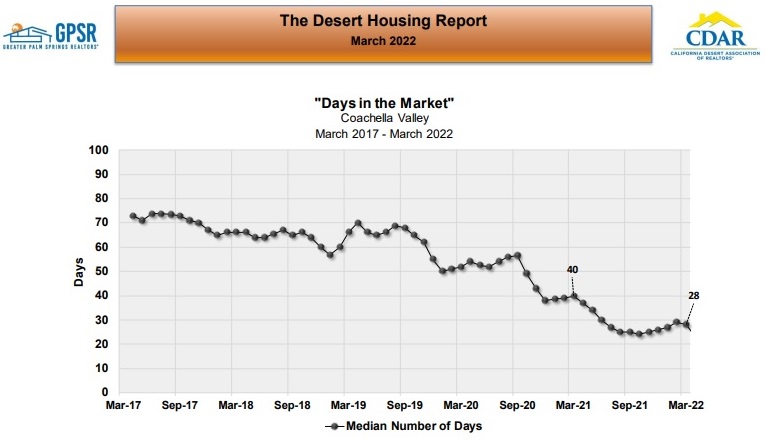

Coachella Valley Overall Days in the Market: At the end of March, the median number of days in the market throughout the entire Coachella Valley was 28 days (one day less than last month and 12 days less than one year ago). Market Watch noted that selling times in the Coachella Valley have ranged between 25 and 30 days for the last 10 months. They explained that with low housing inventory and high home sales, forces continue in place to keep selling times near current, low levels.

Coachella Valley Overall Days in the Market: At the end of March, the median number of days in the market throughout the entire Coachella Valley was 28 days (one day less than last month and 12 days less than one year ago). Market Watch noted that selling times in the Coachella Valley have ranged between 25 and 30 days for the last 10 months. They explained that with low housing inventory and high home sales, forces continue in place to keep selling times near current, low levels.

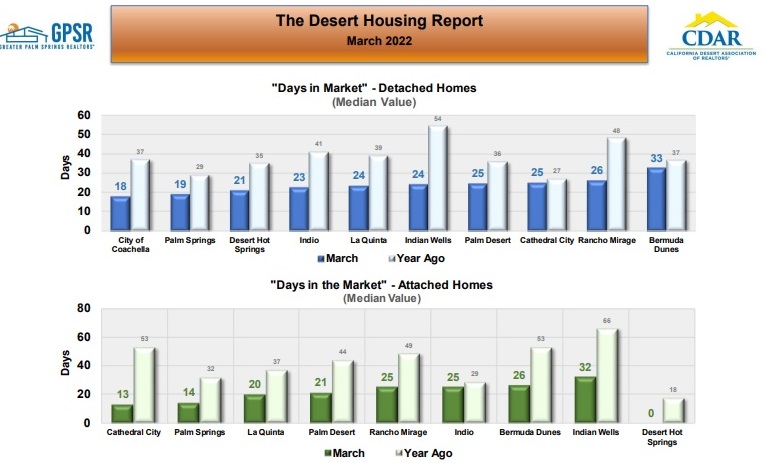

Days in the Market For Detached & Attached Homes By City: In March, Coachella had the lowest selling time for detached homes at just 18 days, followed closely by Palm Springs with 19 days. In March, Cathedral City had the lowest selling time for attached homes at just 13 days, followed by Palm Springs at 14 days.

Days in the Market For Detached & Attached Homes By City: In March, Coachella had the lowest selling time for detached homes at just 18 days, followed closely by Palm Springs with 19 days. In March, Cathedral City had the lowest selling time for attached homes at just 13 days, followed by Palm Springs at 14 days.

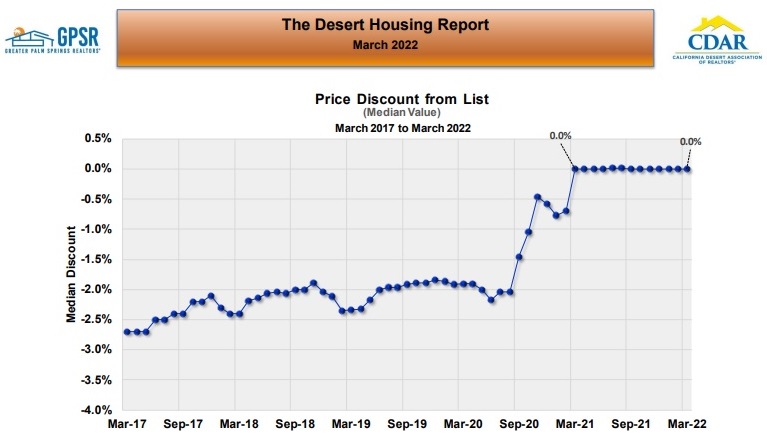

Coachella Valley Overall Price Discount: The median value for sale price discount from list for detached homes in March was again 0.0% (the same as it’s been for 12 months), due to the fact that so many homes are selling at list price.

Coachella Valley Overall Price Discount: The median value for sale price discount from list for detached homes in March was again 0.0% (the same as it’s been for 12 months), due to the fact that so many homes are selling at list price.

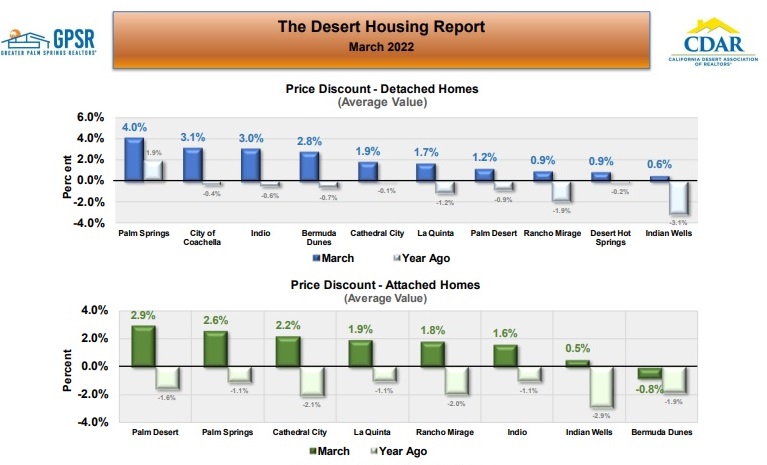

Average Price Discounts For Detached & Attached Homes By City: In March, Palm Springs had the highest selling premium for detached homes at 4%, followed by Coachella at 3.1% and Indio at 3%. In March, Palm Desert had the highest selling premium for attached homes at 2.9%, followed by Palm Springs at 2.6% and Cathedral City at 2.2%

Average Price Discounts For Detached & Attached Homes By City: In March, Palm Springs had the highest selling premium for detached homes at 4%, followed by Coachella at 3.1% and Indio at 3%. In March, Palm Desert had the highest selling premium for attached homes at 2.9%, followed by Palm Springs at 2.6% and Cathedral City at 2.2%

CalDRE# 01898254 | 01896117 | 01991628

CalDRE# 01898254 | 01896117 | 01991628